Also serving the communities of De Luz, Rainbow, Camp Pendleton, Pala and Pauma

Also serving the communities of De Luz, Rainbow, Camp Pendleton, Pala and Pauma

With a strong reduction in the number of homes for sale in Fallbrook this year compared to the last five years, a local expert says it is now a seller’s market for homes priced under $750,000.

“It is a most interesting situation right now,” said Chris Hasvold, owner/partner of Coldwell Banker Landmark Group.

Hasvold said the basic law of supply and demand has led to the shift in the market.

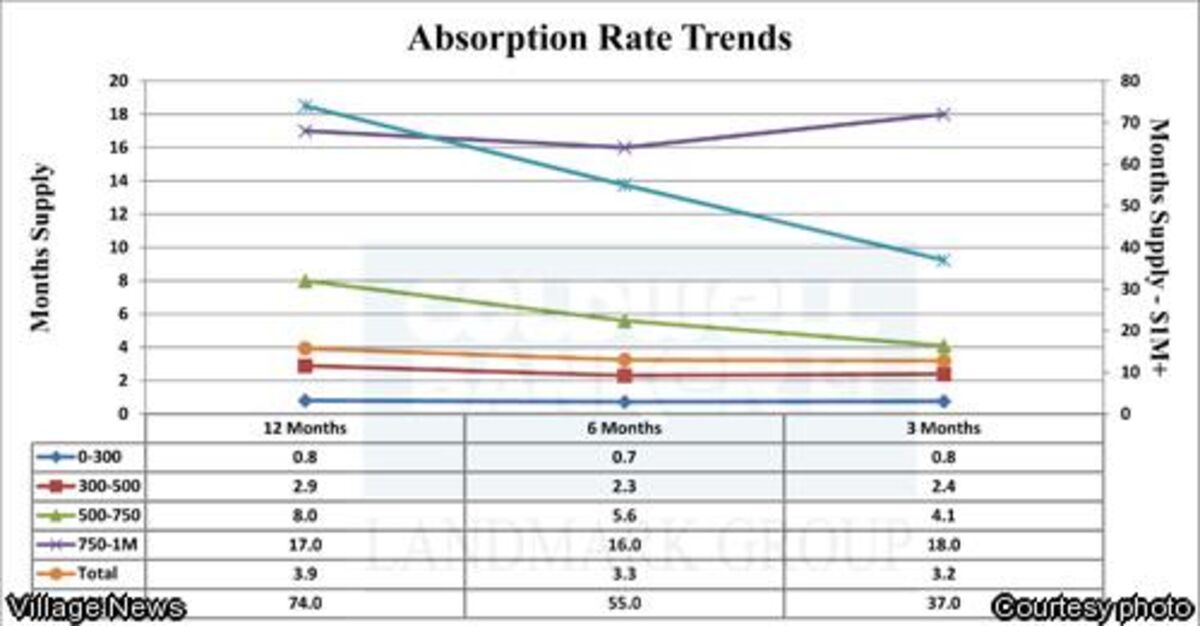

“In real estate, it is determined by what is known as ‘absorption rates’,” he explained. “Absorption rates are best explained like this - only so many houses are going to sell over a certain time – it is a calculation of the supply and demand – and it’s an accurate way to keep track of the trends in the market.”

“A balanced market is when you have a six month supply of homes in a given price range; that means there is enough inventory to supply the demand and you have neither a buyer’s market or seller’s market,” said Hasvold.

“If you have less than six month supply of homes in a price category, it becomes a seller’s market; if you have an over six-month supply, it’s a buyer’s market,” he explained.

Hasvold said homes offered at $300,000 or under have been moving quite well for some time, as most people know.

“We know those go quickly, for the last three months we have only had an average of a three-week supply on hand because there is so much demand for that price segment,” he noted.

In the $300,000 to $500,000 price range, Hasvold said a 2.5 month supply exists currently.

“The supply in that price range has been pretty consistent throughout 2012,” he said.

What Hasvold finds the most encouraging however is what has happened in the $500,000 to $750,000 price range.

“Twelve months ago, we had an eight month supply in that category and that was a buyer’s market,” he said. “Now there is a four month supply.”

Hasvold said there are “significantly more homes selling in the $500,000 to $750,000 category than a year ago.”

“That has been the most dramatic improvement in the market,” he said. “I didn’t think it would be that dramatic.”

Due to the economic challenges nationwide, it’s been quite some time since Fallbrook has been a seller’s market.

“We haven’t been in a seller’s market since October of 2005; that’s when our market peaked,” said Hasvold.

Hasvold said the change in the market began becoming apparent in January.

“We really noticed a change then,” he said. “I’ve been doing a lot of work on absorption rates and trends, which is required now on most appraisals. It is one thing to look at comps (comparable properties that have been sold), but today banks want to know how “fast” things are selling.”

One price category, however, remains a buyer’s market.

“We still have a buyer’s market in the $750,000 to $1,000,000 price range,” said Hasvold. However, improvement has been made this year.

“Twelve months ago we had a six year supply of inventory in that price range; in the last six months the supply has reduced to three years,” he said. “While that is a nice trend, that it has been cut in half, it’s still three years; but it’s progress and that’s what we are looking for.”

Hasvold said in today’s market, when a new home is listed at under $750,000 – and priced at market value – a flurry of activity is occurring and multiple offers are not uncommon.

“It all comes down to effective pricing,” he said. “When sellers price their property accordingly, it generates activity.”

Hasvold explained that buyers looking for something valued at $750,000 or less are very familiar with the remaining inventory on the market, so new listings create excitement.

“There is pent-up demand for new listings because many potential buyers have looked at everything that remains on the market; they either don’t like what they have seen or it sold to someone else,” he said.

“When new listings hit the market, if they are priced well, all the agents land on it; the property is shown steadily and the buzz starts; multiple offers are common right now,” he said.

Hasvold said pricing a home correctly in the market is critical when first listing it and advises against the “start high and be willing to come down” philosophy.

“For a seller, it is far better to take advantage of that first two weeks of excitement as a new listing,” he said. “If you do the old “start high” thing, you ultimately end up getting less and the sale taking significantly longer.”

For those homeowners who continue to be “under water” (owe more on their home than it is worth in today’s market), the challenge continues.

“There are a lot of those people who would like to be able to sell their home and downsize, but can’t,” said Hasvold. “In order to sell their home at today’s value, it means a short sale and they wouldn’t have the equity to buy something new.”

Hasvold said that is one contributing factor to the reduced supply of homes currently on the market.

Qualifying buyers for new mortgages is also different today than in the past three years, according to Martine Quiroz, a senior loan officer with Prime Lending.

“Contrary to the debate, the lending guidelines are stricter, but not necessarily bad for consumers,” said Quiroz. “The guidelines are fair; qualified people who deserve loans are getting them. People who haven’t been responsible aren’t getting loans. However, a lot of programs do exist to help first time buyers get into homes today.”

Mortgage rates are very attractive right now, Quiroz said.

“Today (Oct. 4), we are sitting on the lowest rates in history; the FHA interest rate is 3.25 percent and options exist in FHA to include closing costs; the conventional interest rate is 3.37 with zero points currently,” he said. “It’s a wonderful time to buy a home.”

In qualifying for a mortgage, Quiroz said the consumers most affected by the tighter requirements are the self-employed.

“Those are the folks who during the [housing] boom were the beneficiaries of stated income loans,” he explained. “Those who own a business with $200,000 annual revenue may only show a net of $50,000 after all their write-offs. Unfortunately, the net is what is considered their income for qualifying purposes.”

Quiroz said the best thing a potential home buyer in that situation can do is sit down with an accountant and “create a strategy for showing more income.”

“In other words, they need to prepare themselves to be a better candidate for a mortgage lender,” said Quiroz.

Taking the time to go through the pre-qualification process is very important for a buyer looking to finance a home.

“Pre-qualifying is very important on two levels,” said Quiroz. “First, it is important to look at the client’s budget, cash available for a down payment and closing costs, and a payment that would work for that individual or family.”

Quiroz said the question about a workable payment “wasn’t asked during the boom.”

“It’s not a question of how high of a purchase you can qualify someone for, but what that family can really afford,” he said. “It’s important to select the right loan program for their needs and make sure there is money being left in savings or checking as a reserve, for emergencies. A lot of foreclosures happened because people were cash poor at escrow closing time.”

The second important aspect of pre-qualifying is creating a buyer who has weight in this market when inventories are lower.

“In this very tight market, sellers are carefully screening offers by potential buyers,” explained Quiroz. “We are often preparing cross-qualification packages for people so when they present an offer on a home, it includes their proof of credit, income, credit scores, and more so that the seller knows they are a good buyer to choose.”

Taking the time to pre-qualify has another positive aspect as well, Quiroz said.

“The other benefit is that it also saves the Realtors a lot of time, because they know exactly which type of home the buyer will qualify for. It saves everyone time and money.”

Reader Comments(0)